With yesterday’s action by the Fifth Circuit Court of Appeals effectively unwinding the Department of Labor (DOL) Fiduciary Rule, financial institutions now only become investment advice fiduciaries to retirement plans subject to the Employee Retirement Income Security Act of 1974, as amended (ERISA) and individual retirement accounts if they satisfy the original five-part test, a higher threshold (for becoming a fiduciary) to be sure. While the road to the Fifth Circuit officially vacating the Fiduciary Rule unnerved some, we urged calm, and believe that a measured approach continues to work best.

As a reminder, under the five-part test, one becomes an investment advice fiduciary under ERISA if he or she (1) provides advice as to the value of securities or other property, or makes recommendations as to the advisability of investing in, purchasing or selling securities or other property, (2) on a regular basis, (3) pursuant to a mutual agreement, arrangement, or understanding with the plan or a plan fiduciary, that (4) the advice serves as a primary basis for investment decisions with respect to plan assets, and where (5) the advice is individualized based on the particular needs of the plan or IRA.

With the Fiduciary Rule now just a memory, various firms’ fiduciary status is likely to change, particularly around rollover recommendations. Because of this, we continue to recommend:

- Inventorying the type and nature of typical communications with retirement investors (e.g., other fiduciaries, plan participants, IRAs, etc.) and tagging those that might no longer be fiduciaries under the five-part test.

- Identifying any representations, disclosures or statements regarding fiduciary status that were made in light of the Fiduciary Rule’s scope, which may at some point need correction.

- Re-examining what changes were made to internal policies and procedures to account for the Fiduciary Rule, particularly as state regulators have used non-compliance as a basis for blue sky law violations.

- Reconsidering any revisions to contracts in order to satisfy the DOL’s guidance on 408(b)(2) disclosures that it issued last August.

- Re-evaluating whether to continue excluding small plans and IRAs from investing in private funds, if that determination had been made to prevent a fund manager from inadvertently becoming an investment advice fiduciary to an IRA investor or small plan during the sales and subscription process.

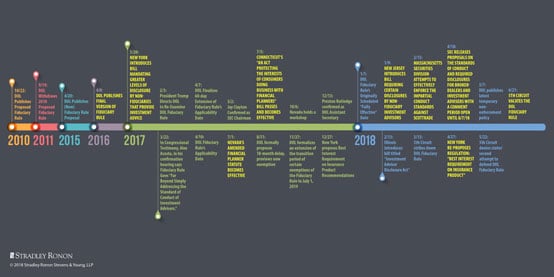

But the DOL is not the only show in town. Fiduciary rulemaking over retail advice continues to evolve, as we highlight in the timeline below.

(Click image to enlarge)

Firms continue to comb through the Securities and Exchange Commission’s (SEC) standard of conduct release. Investment advisers, for instance, may be seeking clarity from the SEC on its proposed Interpretive Release on the extent to which the adviser may satisfy its fiduciary duties through disclosure. Both broker-dealers and investment advisers are also considering the extent to which proposed Form CRS would help alleviate investor confusion.

The SEC also proposed (A) to require broker-dealers and investment-advisers to prominently disclose their registration status; and (B) to restrict standalone broker-dealers and their financial professionals from using the terms “adviser” and “advisor” as part of their name or title. These proposed changes are part of greater scrutiny by federal and state regulators over the titles financial professionals use that could confuse investors as to the nature of the relationship, which has been the focus of a number of state legislatures. Interestingly, the states are taking different approaches to title reform.

Various bills, including New York’s Investment Transparency Act, which either attempt to impose fiduciary status and other heightened obligations on federally-regulated broker-dealers and investment advisers or seek enhanced disclosure of whether a firm is acting in a fiduciary capacity, are advancing. Some of these bills interplay with the SEC standard of conduct release with the prospect that the risk associated with these bills will not be known until the SEC finalizes its standard of conduct release, assuming SEC Chair Jay Clayton can garner enough votes from his fellow commissioners.

The Fiduciary Rule may be gone, but it hasn’t been forgotten. Investor confusion over fiduciary status and conflicts of interest have the attention of the SEC and the states.

Information contained in this publication should not be construed as legal advice or opinion or as a substitute for the advice of counsel. The articles by these authors may have first appeared in other publications. The content provided is for educational and informational purposes for the use of clients and others who may be interested in the subject matter. We recommend that readers seek specific advice from counsel about particular matters of interest.

Copyright © 2018 Stradley Ronon Stevens & Young, LLP. All rights reserved.