At an open meeting on November 5, 2019, a majority of the Securities and Exchange Commission (“SEC”) voted to recommend two proposals amending the federal proxy rules.1 Commissioners Robert Jackson Jr. and Allison Herren Lee opposed these proposals.2 The first proposal conditions reliance on certain existing exemptions under the proxy rules by proxy voting advice businesses such as Institutional Shareholder Services (“ISS”) and Glass Lewis, upon compliance with additional conflicts disclosure and procedural requirements, including permitting issuers to review and provide responses to proxy businesses’ reports.3 The second proposal would amend the proxy rules applicable to the submission of shareholder proposals, including enhanced eligibility requirements and more onerous resubmission limits. The components of each of these two proposals are summarized below. Comments on the proposals are due 60 days after publication in the Federal Register.

I. Amendments to Exemptions From the Proxy Rules for Proxy Voting Advice

The first proposal would amend the proxy rules applicable to companies that regularly provide proxy voting advice to asset managers and others (“proxy businesses”), such as ISS and Glass Lewis. The proposed amendments would (1) clarify that proxy businesses’ voting advice constitutes a solicitation, (2) require additional conflict disclosure in voting advice, (3) provide issuers up to two opportunities to review the proxy advice before it is delivered to clients, (4) provide issuers the opportunity to require in the advice that is delivered to clients a hyperlink to the issuer’s views on that advice and (5) enumerate specific examples of what may constitute misleading statements by proxy businesses. The proposed amendments would increase costs for proxy businesses and may shorten the amount of time asset manager clients have to review proxy advice prior to the vote.

- Definition of “Solicitation.” The SEC’s proposal would amend the definition of “solicitation” under Rule 14a-1(l) and Section 14(a) to include any proxy voting advice that makes a recommendation to a shareholder as to its vote, consent or authorization on a specific matter for which shareholder approval is solicited and that is furnished by a person who markets such advice separately from other forms of investment advice and sells such advice for a fee.4 This definition encompasses voting recommendations promulgated under proxy businesses’ benchmark voting policies or sets of guidelines. The SEC emphasized that the definition of solicitation should continue to be construed broadly. However, the SEC clarified that it intended that proxy voting advice furnished by a person such as a broker-dealer or an investment adviser made only in response to unprompted client requests would continue to be excluded under the definition.

- Conflicts of interest disclosures. Proposed Rule 14a-2(b)(9)(i) requires that persons who provide proxy voting advice and rely on the solicitation exemptions in Rules 14a-2(b)(1) or 14a-2(b)(3) provide additional written disclosures about material conflicts of interest in their proxy voting advice to clients.5

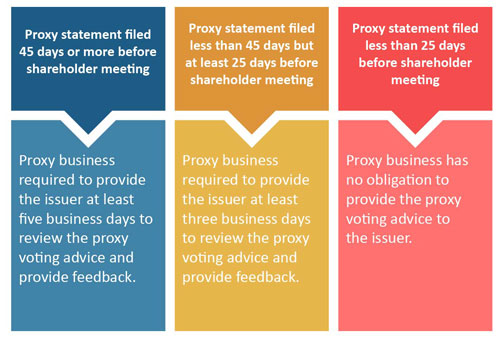

- Timely review and feedback period. Proposed Rule 14a-2(b)(ii), as a condition of relying on exemptive Rules 14a-2(b)(1) and 14a-2(b)(3), would require a standardized opportunity for timely review and feedback by issuers and certain other soliciting persons of proxy voting advice before the advice is disseminated to the proxy business’ clients. This would be required regardless of whether the advice on the matter is adverse to an issuer’s own recommendation, subject to certain conditions.6 The proxy business can condition this receipt of proxy voting advice on the issuer agreeing to keep the contents of the proxy voting advice confidential. The length of time for review and feedback varies depending on how far in advance of the shareholder meeting the issuer has filed a proxy statement (see table below). The proxy business would not be required to accept any suggested revisions. However, in accepting or rejecting any revisions, the proxy business would be subject to Rule 14a-9, which prohibits any materially misleading misstatements or omissions.

- Final notice of voting advice. In addition to the review and feedback period and as a condition of relying on the exemptions in Rules 14a-2(b)(1) and 14a-2(b)(3), proxy businesses would be required to provide a final notice of voting advice to issuers at least two business days prior to the delivery of the proxy voting advice to their clients. This is required regardless of whether the issuer commented on the version it received during the review and feedback period. This final notice should contain a copy of the proxy voting advice that the proxy business will deliver to its clients, including any revisions to the advice as a result of the review and feedback period. As in the review and feedback period, proxy businesses can condition an issuer’s receipt of the proxy voting advice on the issuer keeping the contents of the proxy voting advice confidential.

- Hyperlink to issuer’s statement. Under proposed Rule 14a-2(b)(9)(iii), as a condition of relying on the exemptions in Rules 14a-2(b)(1) and 14a-2(b)(3), a proxy business must, upon request, include in its proxy voting advice and in any electronic medium used to deliver the advice a hyperlink (or other analogous electronic medium) that leads to a written statement by the issuer about its views of the proxy business’s voting advice, regardless of whether the advice is consistent with the issuer’s recommendation. Thus, asset managers relying on proxy voting advice could be confronted with conflicting views of facts or analysis in such advice with very little time to evaluate and determine whether such disagreements should impact the asset manager’s decision on how to vote. Notably, the SEC requested comments on whether proxy businesses should be required to disable the automatic submission of votes unless a client clicks on the hyperlink and/or accesses the issuer’s response or otherwise confirms any prepopulated voting choices before the proxy business submits the votes to be counted. Moreover, an asset manager’s determination to vote in accordance with a proxy business recommendation when such recommendation is subject to an issuer written statement could be subject to increased scrutiny.7

- Anti-fraud provisions. Currently, Rule 14a-9 prohibits any proxy solicitation from containing false or misleading statements or omissions with respect to any material fact. Proposed Rule 14a-9 would elaborate on the current examples of what might constitute misleading information by including failure to disclose information such as the proxy business’s methodology, sources of information and conflicts of interest.

II. Procedural Requirements and Resubmission Thresholds Under Rule 14a-8

The second proposal would amend the shareholder proposal process to (1) provide a tiered approach for eligibility, (2) require certain documents when a proposal is submitted by a shareholder representative, (3) require shareholder-proponents to state when they would be able to meet with the issuer with respect to the proposal and (4) clarify that each shareholder may submit one proposal to an issuer for a particular shareholder meeting.

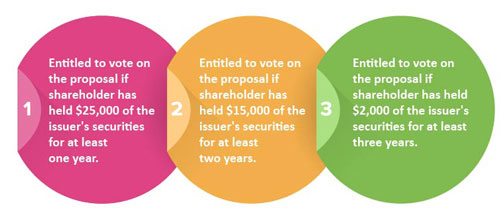

- Ownership Eligibility Requirements. Currently, Rule 14a-8 requires a shareholder to have continuously held at least $2,000 in market value or 1% of the issuer’s securities for at least one year by the date the proposal is submitted. Under the proposed amendments, a shareholder would be able to submit a Rule 14a-8 proposal if the shareholder satisfies one of the three following continuous ownership requirements.

Shareholders would not be allowed to aggregate their securities with other shareholders’ securities to meet the minimum ownership thresholds. This tiered approach reflects the SEC majority’s understanding that a shareholder’s long-term investment in an issuer’s securities makes it more likely that a shareholder’s proposal is meaningful to the issuer and not for personal gain.

- Co-filing/co-sponsoring shareholder proposals. Under the proposed rules, shareholders would be able to continue to co-file or co-sponsor shareholder proposals as a group if each shareholder in the group meets the eligibility requirements.

- Use of a representative to submit a shareholder proposal. To address issuers’ concerns about whether a shareholder truly supports the proposal submitted on his/her behalf, proposed amendments to Rule 14a-8 would require shareholders who use representatives to submit their proposals or otherwise act on their behalf in connection with the proposal to provide the issuer with written documentation confirming the representative has authority to act on behalf of the shareholder.

- Shareholder engagement with the issuer. The SEC proposal also would require a statement from each shareholder-proponent that he/she is able to meet with the issuer in person or via teleconference no fewer than 10 calendar days nor more than 30 calendar days after submission of the shareholder proposal. The shareholder would also be required to include contact information, business days and specific times that he/she is available to discuss the proposal with the issuer.

- One-proposal limit. Rule 14a-8(c) currently provides that each shareholder may submit no more than one proposal to an issuer for a shareholders’ meeting. The SEC proposed amendments to address issuer concerns that proponents try to evade the one-proposal limitation, for example, by a shareholder submitting a shareholder proposal in its own name and simultaneously serving as a representative to submit a different proposal on another shareholder’s behalf for consideration at the same meeting.

- Resubmissions. Currently, under Rule 14a-8(i)(12), an issuer can exclude a proposal if the matter was voted on at least once in the past three years and did not receive at least (i) 3% of the vote if previously voted on once, (ii) 6% of the vote if previously voted on twice or (iii) 10% of the vote if previously voted on three or more times. The proposed amendments to the resubmission thresholds would raise the current resubmission thresholds from 3%, 6% and 10% to 5%, 15% and 25%.8 Shareholders would be allowed to resubmit substantially similar proposals after a three-year “cooling-off” period.

- “Momentum” requirements. In addition to the proposed amendments to the resubmission thresholds, the SEC proposed to amend Rule 14a-8(i)(12) to allow issuers to exclude proposals dealing with substantially the same subject matter as proposals previously voted on by shareholders three or more times in the preceding five calendar years that would not otherwise be excludable under the proposed 25% threshold if (i) the most recently voted-on proposal received less than a majority of the vote cast and (ii) support declined by 10% or more compared to the immediately preceding shareholder vote on the matter. The proposal stated that the purpose of the amendment is to relieve management and shareholders from repeatedly considering proposals in which shareholder interest has declined.

III. Conclusion

With regard to the first proposal, the SEC would permit a one-year transition period after publication of the final rule in the Federal Register. Issuers receiving shareholder proposals for 2020 annual meetings should continue analyzing proposals under existing rules. Interested parties are encouraged to express their views during the 60-day comment period.

The two proposals are part of the SEC’s ongoing work to “enhance the accuracy, transparency and effectiveness of our proxy voting system.”9 The split vote on the proposals, however, reflects the ongoing debate over shareholder engagement. In particular, Commissioners Jackson and Lee expressed concerns that the proposals “shift power away from shareholders and toward management” and limit investors’ ability to “hold corporate insiders accountable.”10

1 Amendments to Exemptions from the Proxy Rules for Proxy Voting Advice, Release No. 38-87457 (Nov. 5, 2019); Procedural Requirements and Resubmission Thresholds under Exchange Act Rule 14a-8, Release No. 34-87458 (Nov. 5, 2019).

2 Robert J. Jackson Jr., Commissioner, SEC, Statement on Proposals to Restrict Shareholder Voting (Nov. 5, 2019); Allison Herren Lee, Commissioner, SEC, Statement on Shareholder Rights (Nov. 5, 2019).

3 Rule 14a-2(b)(1) exempts solicitations by persons who do not seek the power to act as proxy for a shareholder and do not have a substantial interest in the subject matter of the communication beyond their interest as a shareholder. Rule 14a-2(b)(3) exempts proxy voting advice furnished by an adviser to any other person with whom the adviser has a business relationship.

4 The SEC’s proposed amendment would codify the definition from its recent proxy interpretation. Commission Interpretation and Guidance Regarding the Applicability of the Proxy Rules to Proxy Voting Advice, Release No. 34-8671 (Aug. 21, 2019). The interpretation is subject to a lawsuit by Institutional Shareholder Services (“ISS”), which argued that proxy voting advice is not a solicitation. In addition, ISS challenged the interpretation on procedural grounds. Complaint, Institutional S’holder Servs. Inc. v. SEC, No. 1:19-cv-03275 (D.D.C. Oct. 31, 2019).

5 Currently, proxy businesses relying on the exemption under Rule 14a-2(b)(3) provide conflicts of interest disclosures, for example, on their websites. However, in its proposal, the SEC asserted these disclosures may be inadequate because they are often vague or boilerplate.

6 Proxy businesses would not be required to extend the timely review and feedback period or provide the final notice to persons conducting solicitations that are exempt pursuant to Rule 14a-2 or to shareholder-proponents who submit proposals pursuant to Rule 14a-8 and whose proposal will be voted upon at the issuer’s upcoming meeting.

7 In particular, the SEC’s recent guidance regarding proxy voting responsibilities of investment advisers includes a statement that for an investment adviser to form a reasonable belief that its voting determinations are in the best interest of the client, it should conduct a reasonable investigation into potential factual errors. Commission Guidance Regarding Proxy Voting Responsibilities of Investment Advisers, Release No. IA-5325 (Aug. 21, 2019).

8 Specifically, Rule 14a-8(i)(12) would provide that a shareholder proposal may be excluded from an issuer’s proxy material if “the proposal addresses substantially the same subject matter as a proposal previously included in the issuer’s proxy materials within the preceding five calendar years, and if the most recent vote occurred within the preceding three calendar years and was: (i) less than 5 percent of the votes cast if previously voted on once; (ii) less than 15 percent of the votes if previously voted on twice; and (iii) less than 25 percent of the votes if previously voted on three times or more.”

9 Jay Clayton, Chairman, SEC, Statement of Chairman Jay Clayton on Proposals to Enhance the Accuracy, Transparency and Effectiveness of Our Proxy Voting System (Nov. 5, 2019).

10 See supra note 2.

The authors would like to thank Aliza Dominey for her assistance in preparing this alert.

Information contained in this publication should not be construed as legal advice or opinion or as a substitute for the advice of counsel. The articles by these authors may have first appeared in other publications. The content provided is for educational and informational purposes for the use of clients and others who may be interested in the subject matter. We recommend that readers seek specific advice from counsel about particular matters of interest.

Copyright © 2019 Stradley Ronon Stevens & Young, LLP. All rights reserved.